US BDC portfolios contract sharply as gross fundings hit two-year low

LCD data reveals the top 12 US business development companies saw gross fundings fall to $5.7bn in Q1 2026, driven by strategic share buybacks and widening credit spreads.

Top US business development companies (BDCs) reported a significant contraction in their portfolios during the first quarter of 2026, with gross fundings for the 12 largest publicly traded lenders falling to approximately $5.7 billion. According to data tracked by LCD, this figure represents the lowest level recorded since the firm began monitoring the sector two years ago, marking a sharp decline from $9.1 billion in the fourth quarter of 2025 and $8.4 billion in the first quarter of 2025.

The contraction was driven by a steep drop in new investment activity and markdowns that reduced the fair value of existing assets. Several major lenders prioritised returning capital to shareholders over deploying new funds. Golub Capital BDC saw gross fundings shrink 96 per cent year-on-year to just $15 million, with CEO David Golub stating the company had prioritised share buybacks over new investment commitments. Similarly, FS KKR Capital Corp. and MidCap Financial Investment Corp. each saw their gross fundings sink by roughly 75 per cent year-on-year, committing to aggressively buy back their own shares below net asset value rather than seek new debt investments.

Only one of the top lenders increased its gross funding volume year-on-year: Ares Capital Corp., which reported roughly $3.4 billion in new deployments. This was down from $4.8 billion in the prior quarter but remained above the $2.8 billion deployed in the first quarter of 2025. Speaking on an April 28 earnings call, Ares Capital Corp. CEO Kort Schnabel pointed to heightened capital markets volatility, geopolitical uncertainty, and net outflows from retail products, which he said had exacerbated an already seasonally slow market period.

Overall, the top BDCs reported net outflows of $2.1 billion in the first quarter, the largest such outflow since LCD began tracking this data two years ago. This follows a combined $323 million in outflows in the fourth quarter of 2025, marking the second consecutive quarter of net outflows. While net outflows reached $2.1 billion, the fair value of the top lenders’ portfolios fell by $3.5 billion, reflecting the additional impact of markdowns on existing portfolio assets.

Many BDCs marked down loans to software companies and other borrowers to reflect widening spreads in public markets. FS KKR disclosed that it had written down its own net asset value by 10 per cent in the first quarter, driven in part by markdowns on Medallia and other non-performing investments. Medallia was moved to non-accrual status as the company undergoes a restructuring, with lenders further marking down loans that were already significantly impaired.

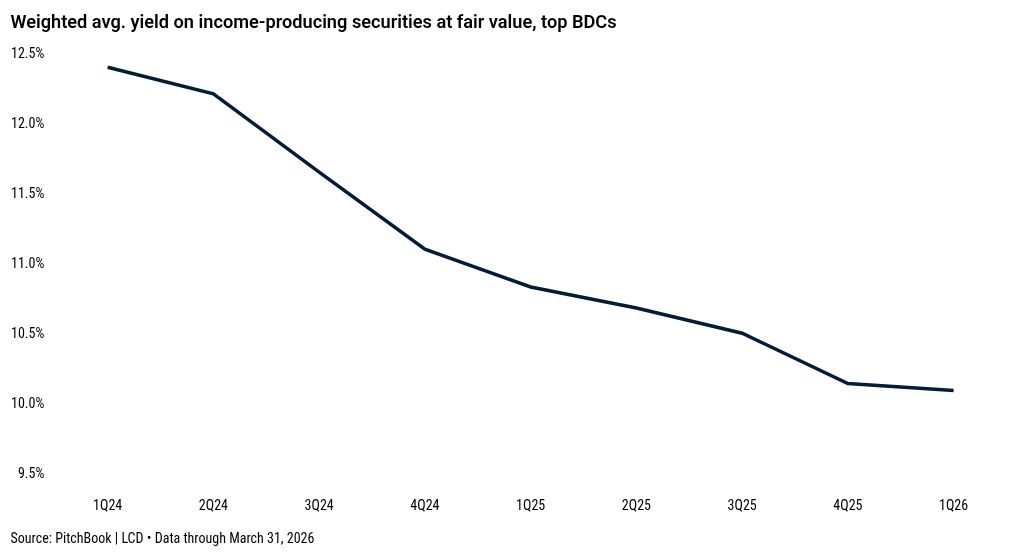

In a bright spot for lenders, portfolio yields showed signs of stabilisation. The weighted average yield on income-producing securities among the top BDCs was 10.09 per cent in the first quarter, a decrease of just five basis points from the previous quarter. A large part of the deployment stems from fourth-quarter transactions that closed in the first quarter, which were committed at spreads lower than those prevalent in the market today. With most BDCs reporting considerably wider spreads in the current market, the decline in portfolio yields is bound to reverse in the coming quarters.