Software sector cedes dominance in US leveraged loan market as healthcare rises

A structural shift in the $1.5 trillion US broadly syndicated loan market sees software companies account for just 9% of new issuance, while healthcare claims the top spot with a record 14% share.

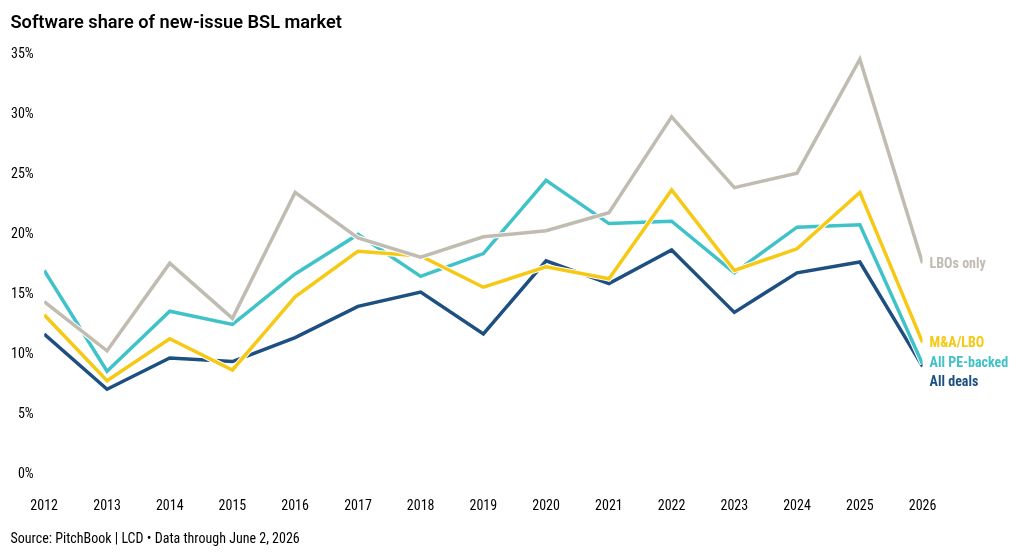

Software companies accounted for just 9% of US broadly syndicated leveraged loan issuance in 2026, marking the lowest share since 2013 and roughly half the volume seen in 2025. This decline signals the end of the software sector's two-decade dominance in the leveraged lending market. Healthcare has risen to claim the top spot in institutional loan issuance for the first time since 2015, accounting for a record 14% of volume in 2026.

The pullback is particularly stark within the private equity-backed universe, where software’s share has collapsed to 9% from 21% in 2025 and a 24% peak in 2020. Engin Okaya, managing director at PGIM Credit, described the sector as among the "have-nots" in a market defined by execution quality. He noted that deals involving complicated business models or characteristics the market disfavors are struggling to gain traction.

Software deals had previously peaked at 34.5% of all leveraged buyout-related financing in the US broadly syndicated loan market last year. However, that share has since fallen to 17.5%, a level not seen in a decade. Milwood Hobbs Jr., deputy chief investment officer of Oaktree’s strategic credit platform, attributed the shift to decreased capital availability and a lack of mergers and acquisitions activity. He stated that private equity firms are being highly selective, and financing conditions are likely to remain challenged.

Healthcare borrowers raised $25 billion from the broadly syndicated market this year, though this figure was heavily concentrated in two January mega-deals: a $7.25 billion term loan for the Hologic buyout and a $4.4 billion facility for an Ensemble Health Partners dividend recapitalization. These two transactions accounted for nearly half of the sector’s total volume. In terms of deal count, healthcare rose to 8.8%, second only to professional and business services.

The rotation away from software is beginning to impact the composition of the broader market. Software remains the top sector in the Morningstar LSTA US Leveraged Loan Index with a 12.5% share, but this is down from a peak of 13% in May 2025. The sector’s outstanding loan portfolio is shrinking as borrowers pay down debt and refinancing becomes increasingly difficult due to higher interest rates, AI-related threats, and reduced private equity appetite.

Eight software borrowers have fully paid down term loans so far this year, including Worldpay, whose acquisition by Global Payments removed roughly $5 billion in par amount outstanding from the index. Software also faces a heavier near-term maturity profile, with 21% of outstanding loans in the sector maturing in 2028 compared with 14% on index loans broadly.

Lenders are demanding better pricing and tighter covenants as they reassess the sector’s risk profile. An early read of the Loan Syndications and Trading Association’s Private Credit Market Sentiment Survey found that more than half of respondents are actively reducing their allocation to the sector. Borrowers with looming maturities may need to rely on amend-and-extend deals or strategic sales to navigate the changing landscape.