Alico posts Q2 profit as land sales and Corkscrew approval drive transformation

Stronger liquidity and local planning approval for the Corkscrew Grove East Village project mark a pivotal shift in the company’s strategy, moving away from weather-exposed agriculture toward development and land monetisation.

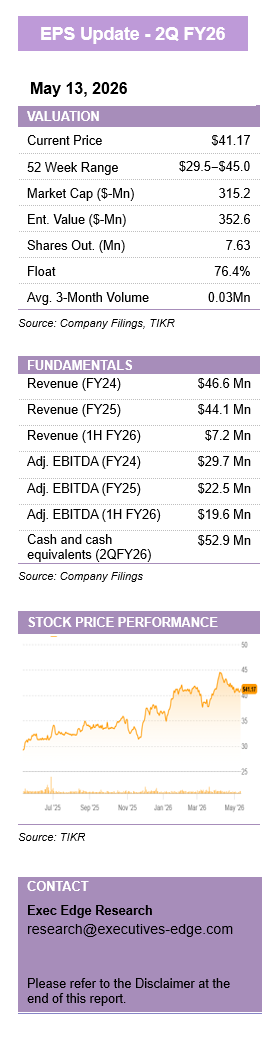

Alico Inc has reported a significant turnaround for the second quarter of fiscal 2026, posting a net income of $11.4 million, or $1.49 per diluted share. This result stands in stark contrast to the $111.4 million net loss recorded in the same period last year, underscoring the company’s accelerated transition from a citrus-focused operator to a land-management and development platform.

The financial improvement was largely driven by the sale of approximately 2,950 acres of non-core citrus acreage for $26.9 million. This transaction brought year-to-date land sales to $34.6 million and provided the liquidity necessary to fund $10.0 million in share repurchases and dividend payments while maintaining a robust cash position of $52.9 million.

Adjusted EBITDA rose 32.6 per cent year-on-year to $16.9 million, supported by lower citrus operating costs and the gains from land monetisation. Total operating revenue fell to $5.3 million from $18.0 million in the prior-year quarter, reflecting the intentional wind-down of the structurally challenged citrus business following the last significant harvest in April 2025.

A key milestone in the company’s long-term strategy was achieved in April when Collier County granted unanimous approval for the Corkscrew Grove East Village project. The approval covers the creation of a stewardship receiving area authorising up to 4,502 dwelling units, including affordable housing and retail space, de-risking the development pathway in Southwest Florida.

With local entitlements secured, Alico’s focus now shifts to securing state and federal permits, with management targeting state approval by early 2027 and federal approval by the end of 2028. The company expects to maintain its FY26 adjusted EBITDA guidance of approximately $14 million, though it anticipates a softer second half as the business model transitions to episodic land sales and development milestones.